Avi Mukesh.

MMath Warwick (First Class, 83%). Software Developer at Singletrack, 4+ years of maths tutoring, and a mathematical finance educator on Instagram.

Built a cross-sectional momentum strategy on cryptocurrencies, an order book simulator in C++, and currently building a Monte Carlo pricing engine in AWS.

Speedcubing and lifting in between.

A cross-sectional momentum

strategy on crypto.

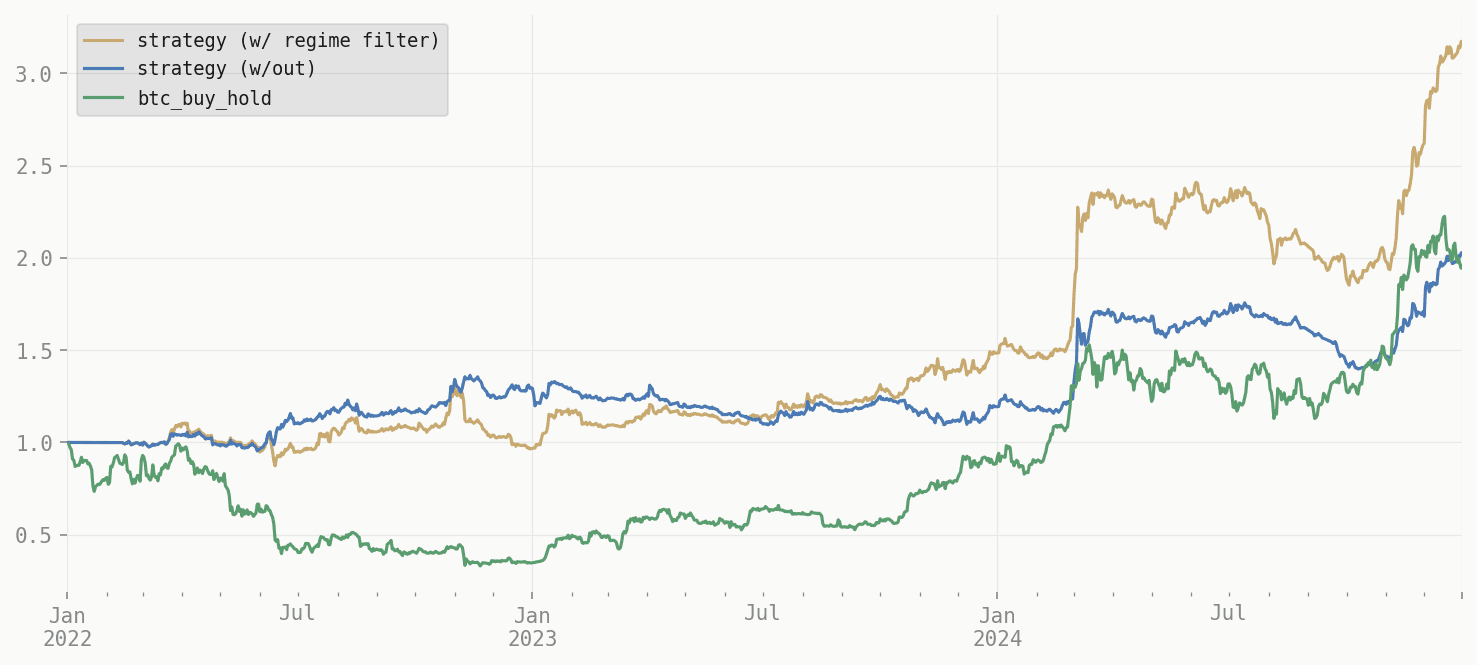

A Python implementation of a cross-sectional price momentum strategy applied to a basket of eight Binance assets. Daily rebalance with a 20bps per-side cost model and a BTC regime filter that zeros short exposure in bull markets. A tweet-attention divergence signal is also explored, with taker imabalance and documented as a cautionary example of overfitting.

Net Sharpe 1.12 in-sample (2022–2024), against BTC buy-and-hold at 0.68 and an equal-weight basket at 0.51. Out-of-sample Sharpe of 0.70 on an expanded 17-coin universe. Near-zero beta confirms the alpha is not simply crypto market exposure.

Tweet-attention divergence showed measurable alpha decay. Information coefficient +0.012 in 2022, decaying to -0.017 by 2024, consistent with increasing market efficiency with respect to social signals.

A BTC regime filter zeros short exposure in bull markets, motivated by the empirical finding that the short leg bleeds consistently during sustained uptrends. Improves risk-adjusted returns across all in-sample years.

Turnover settles at 0.22 at 20bps/side; net Sharpe stays within 0.7 of gross.

A 2D parameter sweep across price and tweet lookback windows shows performance is robust across a broad neighbourhood, not a lucky local optimum.

A secondary price-tweet divergence strategy (in-sample Sharpe 1.56) is documented as a case study in overfitting. It had strong in-sample results that failed to generalise out-of-sample.

Code in the open.

Where I've been.

Outside of work.

A few things I spend time on.